Understanding Forex Trading Tax: A Complete Guide for 2023

Paying Taxes on Your Forex Trades In Australia

In Australia, the ATO (Australian Taxation Office) differentiates forex trading into two distinct categories: investing and trading. It’s an important distinction because it determines whether you need to pay taxes on your ongoing trades – in other words, on the outcome every time you close a forex position – or whether you simply declare your overall investment returns.

Investors are individuals who generate profits from assets or trades held for over 12 months. They are subject to capital gains tax but benefit from a 50% discount. While losses are not tax-deductible, they can be utilized to offset capital gains in the current or future financial years.

Conversely, traders engage in short-term speculative activities involving assets or trades held for less than 12 months. This category typically encompasses most retail forex traders, and their trading income is taxed at their personal tax rates.

Trading income is calculated as profits minus losses and other associated trading expenses. The option to make tax deductibles empowers traders to maintain maximum capital for their ongoing forex trading endeavors.

A Critical Point to Distinguish: Trader or Investor

Trading is now an activity everyone can do – including forex trading. No longer is the strategy of purchasing a currency at a lower price and selling at it a higher one limited to the upper crust of society. Just the same for things like trading on margin to make your exposure – and possible profits – so much bigger.

In the last decade, stock markets, both local and international, have become accessible to just about anyone. This trend has led to a surge of Australians identifying themselves as ‘day traders.’ But what exactly distinguishes a day trader from an investor, and how does this classification affect your tax obligations? Let’s delve into it.

Day Trader versus Investor

According to the Australian Tax Office (ATO), an investor is someone who holds shares with the intent of generating income through dividends. In contrast, a stock (day) trader is described as an individual engaging in business-like activities with the aim of profiting from the buying and selling of shares.

The manner in which you are taxed on capital gains is dependent on whether you’re categorised as a ‘trader’ or ‘investor.’ Being classified as a day trader typically means you’ll be treated similarly to a sole trader conducting business.

How does the ATO classify an Investor or Day Trader?

The ATO is inclined to label you a day trader if your trading behavior includes frequent buying and selling of shares with the aim of profiting. The ATO may also consider factors like volume, regularity, and your record-keeping practices to determine your tax status as a trader rather than an investor.

You can request this clarification from the ATO. In other words, you can get in touch with the tax office and ask them to clarify how your trading patterns and categorized – and, therefore, how you need to pay tax on your trading.

Obtaining an ABN as a Day Trader

Typically, if you classify yourself as a share trader, you’re considered to be carrying out business activities to earn income, which necessitates registering for an Australian Business Number (ABN). You may already have this number – but for many people new to trading, they’d have to register for an ABN.

The ABN is a distinctive 11-digit number that identifies your business to the government and public. It can be used for a variety of tasks, including identifying your business for ordering and invoicing, claiming Goods and Services Tax (GST) credits, and more.

If your turnover exceeds $75,000 per annum (pre-GST), you are obliged to register for GST, which requires an ABN.

Understanding ABN and Business Activity Statements

A Business Activity Statement (BAS), issued by the Australian Taxation Office to all GST-registered entities, records a business’s Goods and Services Tax (GST) activity for a given period. With an ABN, and an annual turnover exceeding $75,000, GST registration and lodging a BAS are mandatory.

For those earning (or expecting to earn) less than $75,000 per annum, GST registration isn’t necessary, and there’s no requirement to submit a BAS.

The due dates for lodging and paying BAS are provided on each issued form. Typically, the due dates are, and the dates are once a quarter – if you file online you receive an extra fortnight to lodge and pay their quarterly BAS.

Tax Rates and Rules

Being registered as a sole trader while day trading, instead of as a company, affects the tax rate you pay. A sole trader operates and manages the entire business, allowing you to follow the individual income rate when filing taxes instead of the corporate tax rate.

Companies are taxed 25-30% on their income, while sole traders pay personal income tax based on their total earnings, including the business’s earnings. The highest personal tax rate currently is 45c in the dollar for income above $180,000.

Sole traders must file personal tax returns, while company owners must file both personal and company tax returns and fulfil the reporting requirements of the Australia Securities Investment Commission.

For both CGT and GST, the same rules apply to sole traders as they do to companies. Sole traders can also apply for small business tax concessions if they meet the eligibility criteria.

Tax Benefits for Day Traders

Being classified as a day trader allows you to offset losses from selling stocks against other profits made during the year, reducing your taxable income. You can also claim several tax benefits enjoyed by businesses.

For instance, any expenses incurred while conducting your trading activities can be claimed as deductions against your total taxable income.

Traders active in overseas markets – which is the case with most forex traders – are treated the same way as trading local shares. The ATO cares more about your permanent residence (i.e., Australia) than where the shares are traded.

Stocks, futures, forex, and cryptocurrencies are all governed by the same ATO guidelines regarding tax. A capital gains tax (CGT) event occurs when you dispose of a cryptocurrency, just as with stocks.

How Can Day Traders Prepare Their Taxes

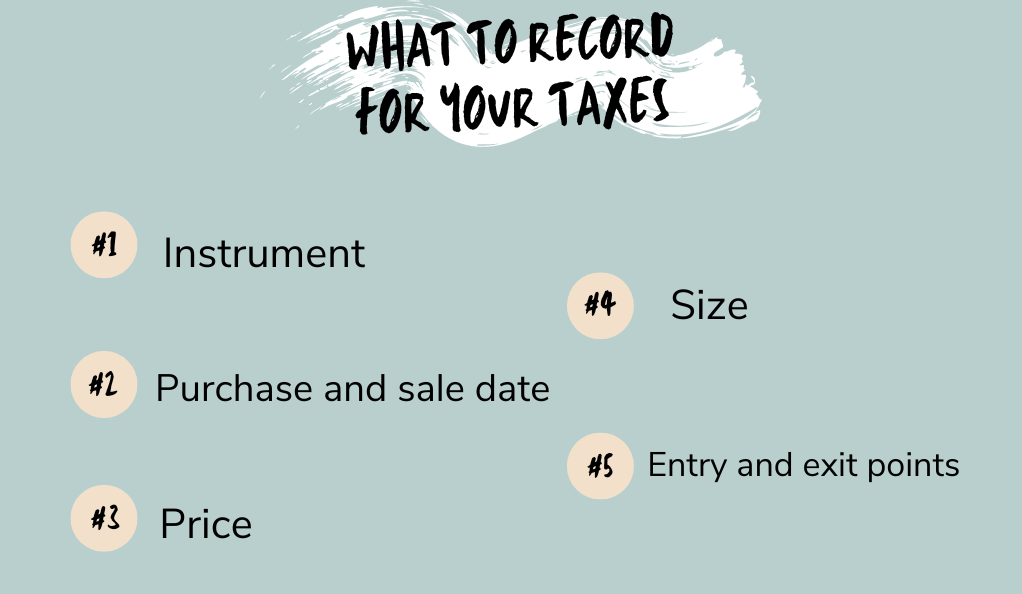

As a day trader, you might make thousands of different trades within a year. The ATO may ask for evidence of all the trades you’ve carried out when submitting your tax return. Whether you prepare your tax return yourself or use an agent, maintain detailed records. For future audits, keep these records for at least five years. Details to keep include:

- Instrument

- Purchase and sale date

- Price

- Size

- Entry and exit points

The ATO also facilitates ‘asset registers,’ allowing you to discard records you might otherwise want to keep. They provide a secure way to store all your trading information. Visit the ATO website for guidance on setting one up.

Use Day Trading Tax Software – And Filing a Return

There’s a variety of sophisticated day trading tax software available that simplifies record-keeping. Many of these products can be linked directly to your brokerage, ensuring that you have all the necessary information when it comes time to file your returns.

Depending on the complexity of your taxes, you might choose to lodge your return yourself or have a professional do it.

You have plenty of options for lodging your Australian tax return:

- With a registered tax agent

- Online with myTax if you’re a sole trader

- With standard business reporting enabled software if you’re a company, trust, or partnership

- By paper

- By mail

When it’s time to pay your tax, the ATO offers various self-service tools and online services to help manage payments. You can pay with BPAY or a credit/debit card, through online payment – using ATO’s Business Portal or myGov account. There’s also electronic transfer or paying by phone, mail or at Australian Post.

The most crucial information at this stage is your Payment Reference Number (PRN), also known as an EFT code. This unique number ensures your payment is credited to the correct account.

Steps To Take to Make Profits and Come Ahead Of Taxes

Acquiring an appropriate broker is a responsibility you must shoulder yourself in order to maximize gains from forex trading. Select a broker who can provide in-depth account details tailored to your investment level.

To find a competent broker, you should thoroughly research their reputation and verify their registration with a renowned authority. Additional considerations should include the leverage level offered by the broker, available withdrawal options, and their commission policies.

Educate Yourself and Sharpen Your Trading Skills

Given the market’s volatility, it’s crucial to comprehend market fluctuations and capitalize on these changes. It’s equally important to understand when to execute a stop-loss order to prevent significant losses.

Use demo accounts to hone your trading skills before venturing into live trading with your hard-earned money. You can find a plethora of updated trading information reflecting the current market trends.

Many international brokers have established educational sections on their platforms to train their traders. For instance, eToro offers an intuitive platform that equips traders with necessary trading knowledge while providing trading services.

Keep a Close Eye on Your Trades

Regularly monitoring your trades and quantifying your success rate in terms of percentages can help assess the profitability of your transactions. For example, an additional income of fifty dollars may hold different value for someone investing a thousand dollars as opposed to someone investing five hundred dollars. It’s vital to treat your forex account like a business account, tracking your returns against the time and resources invested.

Set Profit Goals

Based on your investment, it’s crucial to establish your expected profit margins. Generating profits that correspond with your investment can prevent disappointment when the returns start flowing in.

Defining your profit targets helps you manage your budget and allocate additional funds if needed, particularly if your aim is to elevate your returns, which may require an increased investment. Part of this financial planning might include mitigating substantial losses and ensuring a steady inflow of profits. Investing smaller sums over time can help maintain your budget within manageable levels.

Risks Of Not Paying Your Taxes

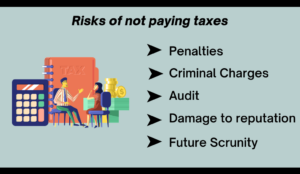

Thinking the Australian government will never find out that you are making profits as a day trader? Think that leaving the profits in your account and not extracting them will keep you out of the hands of the tax authorities. Think again. Here are a few points you need to be aware of when day trading:

- Penalties and interests: The ATO has systems in place to detect undisclosed income, including profits from forex trading. If they discover undeclared income, they can impose penalties and interest charges. The amount of the penalty can be substantial, sometimes equal to the amount of tax owed, and interest can accrue from the date the tax was due to be paid.

- Criminal charges: In severe cases, tax evasion can lead to criminal charges, which can result in fines or imprisonment. The severity of the punishment usually depends on the amount of tax evaded and the intent of the tax evader.

- Audit: Failure to declare income can trigger an audit by the ATO. This is not only stressful and time-consuming, but it can also lead to additional penalties and charges if the audit uncovers irregularities.

- Damage to reputation: If the person is a professional or operates a business, being associated with tax evasion can significantly damage their reputation. This could potentially harm their future business opportunities.

- Future scrutiny: Once you’ve been found to have undeclared income, you may be subject to more intense scrutiny in the future from the ATO. This could mean more frequent and detailed audits, causing inconvenience and additional accounting costs.

Overall it’s simply better to take a careful approach to declaring the profits you make from forex trading – and to declare those taxes to the Australian Tax Office. Yes, it can get complicated, in which case you should consider hiring professional help in the shape of an accountant or tax lawyer. Either way, ensure you declare your taxes on time.

No Comments found